Apke business ko mile #Tarakkeekepankh

Buy Now Pay Later – All You Need to Know

While digital payment services were already on the rise, the pandemic brought about a paradigm shift in the digital payments landscape in India. A sub-industries that is growing phenomenally is buy now, pay later (BNPL) services, especially in the retail B2B space. Our services offer instant, short-term credit to SMBs such as shopkeepers and kiranedaars.

How does BNPL work?

Shopkeepers, dukaandaars, and kiranedaars are the backbone of the Indian retail economy and make up the largest chunk of the retail industry. And even though a huge chunk of the retail business in the country is credit-driven, most of it is informal. The resources that the industry needs to modernize and scale up to have always been beyond its reach. And a significant reason for that has been stunted access to working capital. Our services help small business owners get instant credit to source stock from various PAN-India suppliers at the best prices. Thus, it helps them grow and better profitability.

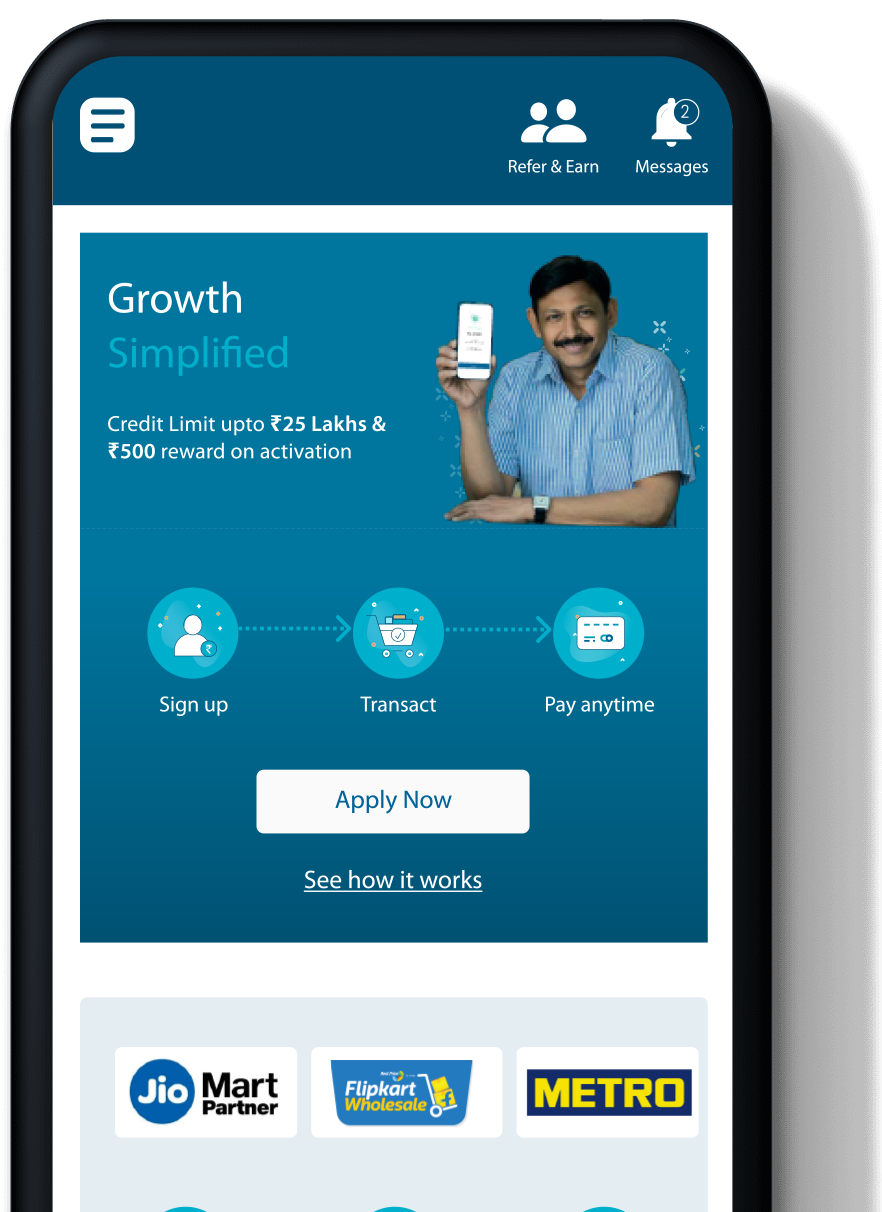

For small-time shopkeepers and dukaandars, bank loans are tedious. They not only take a long time to get approved but also require them to pledge collateral. Shopkeepers don’t need burdensome loans but rather smaller-sized credit products that they can access easily to buy supplies inventory. This is where ePayLater’s services come in. It gives kiranas access to interest-free liquidity, i.e., working capital of up to INR 25 lakhs. Plus, there’s even a 14-day interest-free credit period.

The idea is to allow dukaandars to get credit akin to distributors’ credit but access it via a formal channel not circumscribed by a personal trust. It will enable them to order supplies and inventory from any supplier across India and also get great discounts/schemes. Consequently, this results in the stocking of fast-moving products, more sales, better customer loyalty, higher turnover, and higher profits.

Advantages of BNPL

- Credit for everyone: The kirana is a business segment that deals majorly in cash but doesn’t possess a paper trail for getting credit from formal or traditional sources. Our services employ technology to insert ourselves in the chain. We do so by using the advantage of the commission spread to extend short-term credit to retailers. With the delinquency rate being just 0.15%, this credit innovation is sustainable to the point where it finances not just lifestyles but rather livelihoods.

- Expansion of the credit system: Credit cards have a very small penetration in the country. Our services help more people enter the credit system. Our offerings take much lesser time to get approved as compared to credit cards.

- The rise of the kirana: ePayLater’s services allow 14-30 days on each purchase. Thus allowing shopkeepers to align them with their own working capital cycles. This is hugely beneficial instead of having a single billing date like credit cards. Our services do away with any sort of predatory pricing. They don’t encourage revolving credit either, with the objective being to remove the cost burden from small-time businessmen and retailers. As a company philosophy, ePayLater doesn’t wish to benefit from its borrowers’ inability to pay back the loan on time.

- Combining benefits: ePayLater combines the benefits of buy now, pay later services with that of a credit card. We facilitate dukaandaars and kiranedaars to buy stock from any supplier across India. Since there is no annual or joining fee, setting up an account is very simple, and has can be used PAN India . Our algorithm crunches a lot of useful data and arrives at this unique digital credit solution for the average kirana.

Eligibility criteria for Buy Now Pay Later

Applying for instant credit with ePayLater’s services is very simple. One must be 18 years of age and have an Android smartphone, PAN and Aadhar card. Download the ePayLater app and log in with your mobile number and an OTP. After accepting the ‘Terms and Conditions’, click on ‘Apply Now’ to continue entering your PAN card details. The KYC process with Aadhar and OTP is next to allow access to your Digi locker account. After that, all you need to do is enter your bank and business details, sign the agreement, and register for eMandate to get a pre-approved credit limit of INR 2 lakhs. Your credit limit is approved in a matter of 2-3 business days. If a retailer/dukaandaar applies through the partner merchant portal, then many of these steps can be skipped.

Difference between Credit Card and BNPL

So, what is the difference between credit card and BNPL? As opposed to the mere 2% card penetration in India, BNPL services such as ePayLater are ensuring that a greater number of people become part of the credit system. Furthermore, our services are form-agnostic compared to the plastic nature of credit cards. But, one of the biggest advantages of buy now, pay later is that the process is hassle-free and quick, while credit cards take a lot of time to get approved.

Furthermore, our services allow 14-30 days of interest-free credit on every purchase. Kiranedaars and dukaandaars can easily align their working capital cycles with our interest-free credit cycle, as they don’t have to adhere to a single billing date. Our services don’t intend to make money off of interest on deferred payments, revolving credit, etc., but rather work to eliminate the cost burdens of shopkeepers. The idea is to not take advantage of any inability on their part to pay on time.

Interest rate comparison (Credit card vs. BNPL)

Credit cards are a rather impractical product when it comes to India’s retail business, even though a majority of the business is driven by credit. For one, their approval process is a long and rather daunting one. Secondly, single billing dates don’t exactly match up with working capital cycles when kiranas require money to buy inventory at the rates that they want. If that wasn’t enough, credit cards are very expensive, as they charge everything from annual fees and interest on interest, but even late payment fees.

As compared to that, our services, as we mentioned earlier, offer immediate interest-free credit for 14 days. This allows kirana shops, all eligible credit users, to line up their working capital cycles with the credit we provide. What’s more, our services are easy to set up and use, and we don’t have annual fees either. While we do have a late payment fee, the delinquency rate is less than 2%, which means that this setup works better for kiranas as compared to credit card structures. Essentially, we act as allies to kirana stores, helping them grow sales, customer loyalty, and, consequently, their business by providing them credit without the hassles associated with a credit card.

The Future of Buy Now Pay Later

Half of India’s working population, which is almost 20 crore people, is credit active. Even though credit cards have been around for a long time, the Indian credit card market is still severely under-penetrated. Due to the obstacles ascociated with credit cards, SMBs like Kiranas find it difficult to get their foot in the door. And being excluded from this narrow circle of ‘credit trust’ is a major hurdle for enterprising mom-and-pop establishments that want to grow and expand.

This is where BNPL is poised to be the next big thing in India’s retail B2B space. In fact, BNPL services’ popularity increased by a staggering 600% in 2021, and it’s clear why. Many round-the-corner kirana stores turned to BNPL services during the pandemic looking for credit to extend their stock-buying capabilities. Due to the unpredictability at the time, BNPL services assisted them in obtaining credit at a time when credit was drying up.

ePayLater’s services allow kiranas to defer payments for purchasing stock towards the end of the billing cycle. Our short-term credit solution splits repayments into flexible instalments, and that too without interest for a period of 14 days. With no hidden fees or high-interest charges, the popularity of BNPL services such as ePayLater is growing exponentially.

FAQs on Buy now pay later

How does BNPL make money?

Intermediary services, such as ePayLater, use algorithms to crunch a ton of numbers relating to financial and credit backgrounds. We employ technology that allows us to place ourselves in the middle and earn a commission from suppliers by paying them immediately after delivery. As a result, we use that spread to borrow from banks and extend instant, short-term credit to smaller retailers.

Is buy now pay later an instalment loan?

Yes, BNPL can be considered as a kind of instalment loan, as retailers pay back the credit amount in parts. After an interest-free credit period, in our case 14 days, interest is charged on the amount that retailers borrowed and spent. In case retailers fail to pay back the amount within the stipulated period, the penalty is levied.

Do you pay interest on buy now pay later?

Yes, you will have to pay interest on BNPL services, but only if you don’t pay back the borrowed amount in the interest-free credit period. After the initial credit-free period, we charge a penalty interest of 3% every month from the date of the transaction. There are also be additional charges levied, such as bounce charges if the account balance is insufficient. Additionally, GST is applicable on the late payment charges.

Where can I use the buy now, pay later option?

You can use our services directly via the ePayLater app, any time and from anywhere. After signing up and registering for our services, you can use our facility to make the payment by choosing the supplier you want to make the payment to. Just enter the amount, the invoice number, and a copy of the invoice. Choose your preferred mode of payment (net banking/debit card/UPI), enter the OTP sent to your registered mobile number, and confirm – it’s as easy as that.

Does BNPL affect credit?

As long as one repays the amount on time, one’s credit score won’t be impacted. In fact, clearing the amount on time not only assures you peace of mind but could also improve your credit score. Also, ePayLater doesn’t charge users for pre-payment of credit borrowed. However, if you delay or miss your payments, then your credit score could fall.

For the latest news and updates follow us on Facebook

Top Searches

Recent Articles

-

Tapping The Digital Opportunity For India’s Unorganized Retail To Realize The Atmanirbhar Dream

India’s retail sector contributes about 10%...

Read More -

-

Instant Credit for Business

Apply for ₹25 Lakhs Business credit on ePayLater in just 5 minutes*

Download now!