Apke business ko mile #Tarakkeekepankh

All you need to know about a line of credit

A line of credit allows shopkeepers to access on-demand credit. Neither is it a personal loan nor is it quite a credit card, but it has an edge over both. Instead of one-time fund access, it offers variable access to a personal loan fund. Plus, it has a lower interest rate as compared to credit cards.

A line of credit is of two kinds, secured and unsecured line of credit. One needs to pledge assets they own in a secured line of credit. They typically have lower interest rates and flexible tenures as compared to unsecured loans since there’s collateral. Additionally, if you default on the loan, the lender has the right to sell the collateral to recover any damages.

An unsecured line of credit, like ePayLater’s services, doesn’t require any collateral. This is especially helpful in the Indian retail B2B space, especially for SMBs and small-time retailers such as kirana stores. Since they need bite-sized credit to manage their working capital cycles as opposed to traditional loans or even credit cards, our services have proven to be a boon.

What Is a Line of Credit?

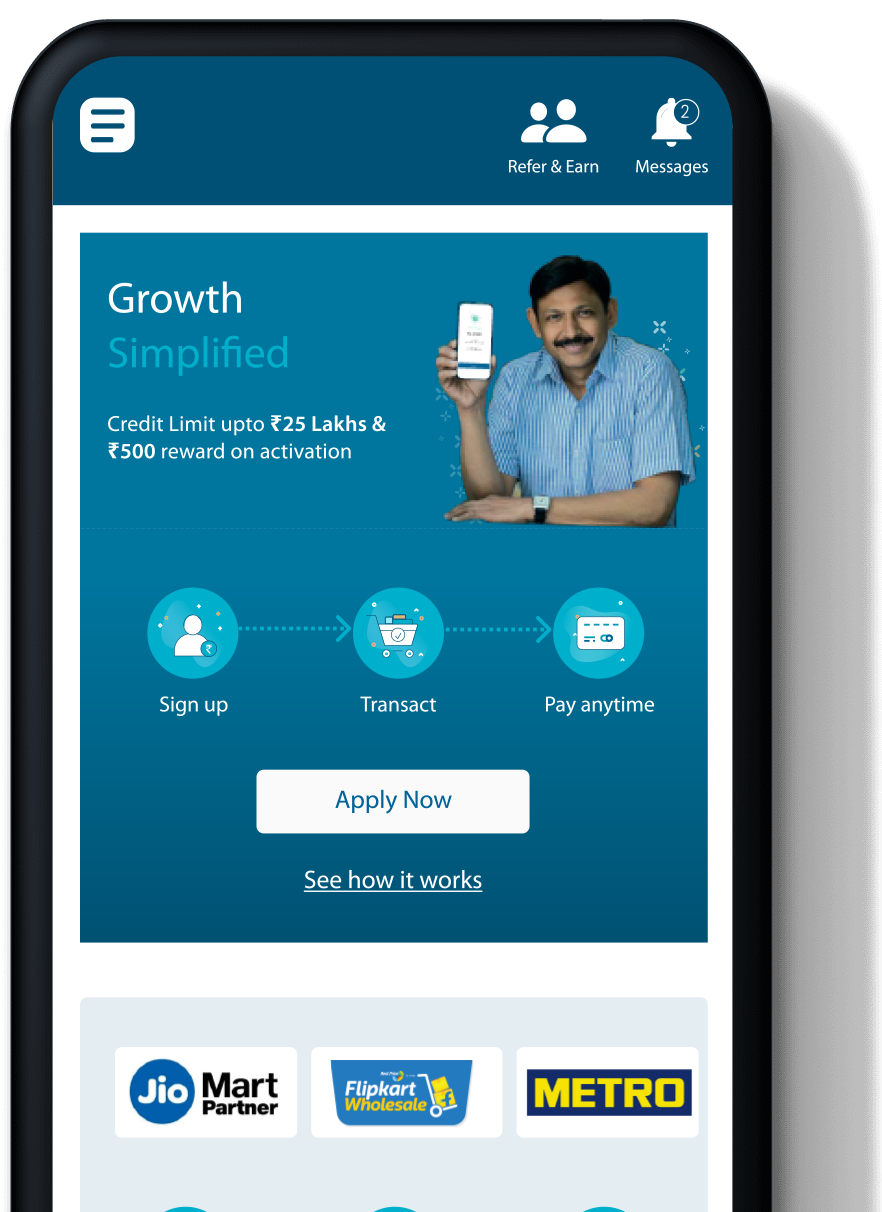

A line of credit works just like a credit card. Without any of the hassles of a credit card, but with the advantage of being able to be used anywhere. Lines of credit, such as ePayLater, are deferred payment solutions that offer retailers interest-free credit of up to ₹25 lakhs. Using this fresh working capital, small-time retailers can enjoy interest-free credit for up to 14 days. They can then use this to purchase inventory and stock up products. So, they can use this credit facility to obtain the best prices and discounts for their inventory. The stores then pass this benefit to the consumer. Consequently, this translates to higher sales and higher profitability.

When a Line of Credit Is Useful

Businesses across all industries were hit severely during the pandemic. This is where line of credit services such as ePayLater began to gain momentum. Retailers found it to be the ideal tool for balancing cash flows and working capital requirements. They no longer had to worry about credit for buying from pan-India suppliers. Additionally they could even avail the best prices and discounts because credit was always available.

What also helps retailers is that in lines of credit, they only pay interest on the amount they use. This allows them to plan stocking schedules, buy inventory at better prices, and also pay off the borrowed amount at any time during the 14 days, in the case of our services.

Unsecured lines of credit services in India have been taking advantage of increased awareness and internet penetration. We’ve helped small-time retailers take advantage of limited-time discounts and prices offered by suppliers. To get the best prices for the stock that you want, ePayLater’s credit is available to you anytime and anywhere. If that wasn’t enough, you have multiple payment options to utilize the line of credit, such as net banking, debit cards, and even UPI.

Consequently, this also helps retailers and small-time businesspeople build their own business credit history.

The Problems with Lines of Credit

In the end, everything boils down to your financial discipline and how well you utilize the line of credit. In case of late payments , we charge a penal interest of 3% every month from the date of transaction. However, since you can make payments anywhere and anytime, all you need to do is maintain sufficient balance on the due date.

An important thing to remember is that a line of credit is as helpful as one makes it. So, a line of credit, such as ePayLater’s instant credit, should only serve as a safety net for cash flow shortages in business. It’s a real temptation to use it for other purposes, and doing so is a recipe for disaster.

Comparing Lines of Credit to Other Types of Borrowing

Credit Cards

- The most significant difference between a line of credit and a credit card is the former allows borrowing credit against a revolving credit line. This is opposed to a lump sum that a loan offers. Alternatively, a credit card enables retailers to make purchases that they could then pay back by a specific billing date. Lines of credit have fixed and typically lower interest rates. Credit cards have higher interest rates, along with different kinds of fees. Both lines of credit and credit cards could be secured or unsecured. Credit cards however, could have reward programs that lines of credit usually do not. That being said, our services even work as an opportunity for buyers, whether small-time buyers or bulk buyers. We also offer a refer and earn program. This goes a long way in helping retailers also build a credit profile and earn profits without any additional investment.

Loans

- Loans have non-revolving credit limits, which means that borrowers can access funds only once as a lumpsum. After that, they make principal and interest payments until the entire amount is paid back. Lines of credit, however, get borrowers access to set credit limits. To pay it back, they make regular payments of both interest and principal. However, in lines of credit, borrowers have repeated and continual access to it until it’s active.

Payday & Pawn Loans

- Pawn loans are cash loans given against collateral such as musical instruments, tools, or jewellery. The amount depends on the item’s value, and is returned to the owner on repayment within the stipulated period. If one fails to do so, the pawnshop can keep the item and put it up for sale. Payday loans, on the other hand, are high-interest loans granted against post-dated cheques. You need to provide recent bank accounts, permanent residence proofs, and payment stubs. Lines of credit such as ePayLater’s are much more straight forward. They do not require collateral or need you to furnish the huge amounts documents that payday loans require.

Line of Credit Types

Personal Line of Credit

- A personal line of credit, which can be both secured and unsecured, allows borrowers to access “on-demand” money. It’s not a personal loan, or a credit card – instead, it’s the best blend of both. Firstly, it has a much lower interest rate than a credit card. This makes it more affordable in terms of cost. Secondly, it allows borrowers to have variable access to funds. They are no longer constrained to one-time, lump-sum fund access.

Home Equity Line of Credit

- Home equity lines of credit, or HELOCs, are variable-rate loans. They allow borrowers to borrow a certain part of the amount that the bank pre-approves. So, just like home loans, the house/residential properties act as collateral in HELOCs. Plus, the monthly payments depend on the amount borrowed and the interest rate. However, unlike home loans, borrowers can re-borrow the amounts after repaying them. Finally, HELOCs have a defined time of repayment by which borrowers must pay back the outstanding balance.

Business Line of Credit

- Business lines of credit are business loans where businesses can borrow up to certain limits and pay interest only on the part of the amounts borrowed. This revolving credit loan is secured against financial assets such as fixed deposits, mutual funds, stocks, etc. The maximum amount that the borrower can obtain is based on the value of pledged assets, business cash flows, and the overall financial condition.

Our services differ from a business line of credit in the way that they don’t require collateral. This allows SMBs to stock better, increase sales, and even expand the business. It is especially helpful for small-time retailers who don’t have credit profiles or collateral to pledge. In such cases, they wouldn’t have been able to sell better or grow without BNPL offerings such as ePayLater’s services.

Uses for Lines of Credit

Since its inception, ePayLater has been empowering retailers, especially the small-time kirana shops around the corner. When the country was locked down and getting essentials was a challenging task, these kiranas were a boon. These small businesses don’t have the advantages that larger firms have. Their infrastructure, scale, or finances, are all relatively limited. ePayLater provides them with the platform to begin their success story. Through interest-free credit of up to INR 25 lakhs for up to14 days they can attain their business dreams.

We’ve partnered with multiple merchants across the country. This includes local distributors, which allows dukandaars to choose the suppliers that they want to purchase stock from. Resulting in them being able to take advantage of the best prices and any possible discounts. With the easily accessible stream of credit shopkeepers can primarily manage their cashflow. In turn they can reduce costs, stock better, increase sales, and consequently, profit margins. Our offerings also help them safeguard against unforeseen circumstances, with the pandemic having been a testament to it.

Kirana stores dominate the retail industry with over 14 million stores across the country. We encourage them to work towards and achieve their dreams without having to worry about accessing credit. Instead, they can focus on growing their business, the industry, and the country, as a result.

ePayLater’s services are a fantastic way for these small-time businesses to build a credit profile. Through which they open the door for larger loans in the future.

Top Searches

Recent Articles

-

Tapping The Digital Opportunity For India’s Unorganized Retail To Realize The Atmanirbhar Dream

India’s retail sector contributes about 10%...

Read More -

-

Instant Credit for Business

Apply for ₹25 Lakhs Business credit on ePayLater in just 5 minutes*

Download now!